In a chapter from the book Finance and the Good Society, Professor Robert Shiller of Yale University penned a metaphorical description drawing the intrinsic symmetries between financial markets and nature in general: “The fact that the real world of financial capitalism is so often messy and inhuman, and that it involves so much hypocrisy and manipulation, may detract from this sense of beauty. But the same is true of all nature. For all its beauty, it produces ugly things as well.”

FINANCE, MATHEMATICS AND BEAUTY

Financial theory, as well as economic theory more generally, can be beautiful. The beauty in markets, likewise with that of nature, is essentially bound by the element of symmetry. This was the key idea behind the concept of the Efficient Market Hypothesis that has widely been adopted and believed by institutions far and wide. As Professor Shiller explains, this is the idea fundamental to financial theory – that prices in different markets are just different manifestations of a deep underlying truth. The apparently meaningless jiggles – or the ‘random walks’ – in price charts are reflective of true economic power. The accumulation through time of these small price changes amounts to a result that is not random but that instead provides discovery of true economic value – a value that is highly useful in the allocation of economic resources and in generating our livelihoods.

LIKE A BLACK HOLE TAKING IN WITHOUT LIMITS

To a certain degree, one can visualise our financial systems and markets as a sphere containing mystical elements that allow it to ingest new matter from the exogenous environment. New matter can manifest itself in the form of new information, such as comments from the Chairman of the Federal Reserve Janet Yellen on the possibility of raising interest rates earlier on triumphant non-farm payroll news, which may potentially act as a game changing factor to decision-making by businesses and financial institutions. Upon taking in this matter unto itself, the sphere may be temporarily altered in size and shape – as such new matter may serve as tremors to the entire economic system which may alter certain intrinsic characteristics – but equilibrium is soon restored. As conceptualised by the Efficient Market Hypothesis, this equilibrium is restored through a process that resembles a negative feedback system, with the exception that the end resultant system is slightly altered in characteristic. During the process, price continues to ‘walk’ in a ‘random’ direction with a general gravitation towards the new equilibrium as established by the new input into the ecosystem.

TWO TALES OF SYMMETRY – STATIC VS FLUX, RANDOM VS DETERMINISTIC

This theme of symmetry in equilibriums that are in a state of flux is also written on today by Mark Buchanan from Bloomberg. In a BloombergView blogpost today, he wrote about how this mechanism is a traditional thinking about market efficiency: “…any deviation from the efficient equilibrium – a momentary mismatch in the prices of two stocks, for example – ought to create incentives for investors to act in ways that will quickly erase that deviation, restoring the equilibrium. The metaphor is of a system in stable equilibrium, like some water in a bowl, which settles down soon after it’s perturbed.”

However, another system proposed by two physicists Felix Patzelt and Klaus Pawelzik argues otherwise. They liken the mechanism to be the act of balancing a stick on one’s finger – Stay vigilant, and whenever the stick departs from the straight-up position, move your finger and hand even further in that direction to compensate. The symmetry lies in the automatic knee-jerk restoration of stability after periods of instability.

This system seems to be more holistic in describing a financial system that operates under the state of “random walk” – when balancing the stick – and intervals of highly deterministic behaviour – drastic rebalancing of fingers to find the centre of gravity – that are characteristic of market crashes. In the blogpost, Mark Buchanan accredits this model with its due mathematical legitimacy: “The erratic instability is reflected in a specific mathematical pattern, a so-called power law reflecting the heightened frequency of abrupt and surprising big movements, as well as their tendency to cluster together in sharp turbulent episodes.”

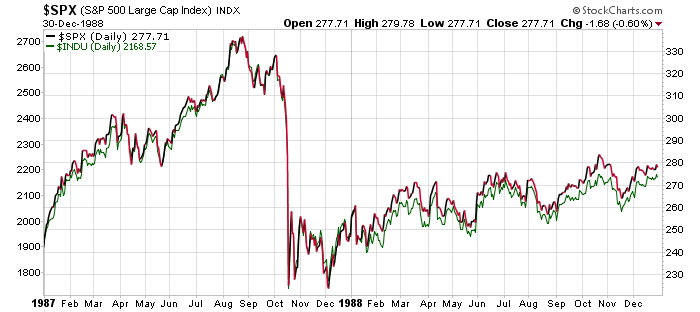

If we were to extend this illustration further, it would also make sense to see why certain “black swans” exist and why highly deterministic events – such as the Black Monday on October 19, 1987 when the S&P 500 index registered its worst daily percentage loss of 20.5%. – a few standard deviations away from the mean in a Gaussian Function can occur with a highly than expected probability.

The S&P 500 Index was random walking – until it subscribed to a highly deterministic force on October 19, 1987

PARALLELS TO SEISMOLOGY

In many aspects, I find close similarities in behaviour between financial markets and seismic activity. Likewise with financial markets, highly deterministic events such as earthquakes occur at intervals of long periods of gentle and mild tremors – which are generally shown on the seismometer by an oscillating needle responding erratically (or randomly) whilst gravitating back to its equilibrium.

After some research, I found a large amount of financial literature that has been authored in this area with most focusing on predicting the risk of downward price movements one-step ahead with measures like Value-at-Risk and Expected Shortfall. A particular study, titled Interpreting financial market crashes as earth quakes: A new early warning system for medium-term crashes adopts an Early Warning System for medium term crashes. By first defining large price movements as a potentially early warning sign – like an out-of-the-blue movement of the seismometer needle with a much greater displacement – the authors of the study then proceeded to find models that capture herd behaviours that cause such disturbances:

“This positive herding behavior causes crashes to be locally self-enforcing. Hence, while bubbles can be triggered by an exogenous factor, instability grows endogenously.”

Then, it is obvious to see how such a self-exciting behaviour can be found in seismic behaviour, where aftershocks can generate new after shocks and so on.

STILL GOT MUCH TO DISCOVER

What is there to make of such literature and parallels? I do not know as yet, but I am sure I will be returning to write on this more elaborately. It is definitely interesting to draw symmetries and similarities between financial markets and the physical nature, as we can see how our penchant for symmetry in concepts of beauty and art drives that very negative feedback loop in restoring markets to equilibrium. However, we have to recognise how this market mechanism is not necessarily intended by individuals that make up the market. The collective effect of all individuals acting in accordance to their own self-interests is the force behind this mechanism – this serves us as a more elusive understanding of how exactly markets function and respond.